When considering a personal loan, one of the most important factors to consider is the interest rate. The interest rate on a loan determines how much you'll pay in addition to the principal amount you borrow. It’s crucial to understand how personal loan interest rates work and how to find the best rate for your financial situation.

In this article, we’ll explore everything you need to know about personal loan interest rates, how they’re calculated, and how to secure a competitive rate.

What are Personal Loan Interest Rates?

A personal loan interest rate is the percentage of the loan amount that a lender charges you for borrowing money. Interest is typically paid in installments, with the amount added to your monthly payments over the term of the loan.

The interest rate on a personal loan depends on several factors, including:

- Your credit score

- Income and employment history

- Debt-to-income ratio

- Loan amount and term

- The lender's policies

In general, the better your credit score and financial standing, the lower the interest rate you can secure.

Types of Personal Loan Interest Rates

There are two main types of interest rates associated with personal loans:

- Fixed Interest Rate:

- With a fixed-rate loan, the interest rate remains the same throughout the life of the loan.

- This means your monthly payments will be consistent and predictable, making it easier to budget.

- Fixed-rate loans are typically preferred by borrowers who want stability and long-term planning.

- Variable Interest Rate:

- A variable-rate loan’s interest rate can change over time, typically in response to fluctuations in a benchmark interest rate, such as the prime rate or LIBOR (London Interbank Offered Rate).

- While variable rates are often lower at the outset, they can increase over time, potentially leading to higher monthly payments.

- Variable rates can be beneficial if you anticipate a decline in interest rates or if you’re planning to pay off the loan quickly.

How are Personal Loan Interest Rates Calculated?

Personal loan interest rates are usually determined by the lender based on the annual percentage rate (APR). The APR is the total cost of borrowing, including both the interest rate and any fees associated with the loan.

The APR may include charges such as:

- Origination Fees: A fee charged by the lender for processing the loan.

- Late Payment Fees: Charges incurred if you miss a payment.

- Prepayment Penalties: Fees charged for paying off the loan early (although many lenders no longer charge this).

Your APR will be higher if you have a poor credit score or if you're borrowing a higher amount for a longer term. Lenders will also take into account your creditworthiness (a combination of your credit score, history, and other financial factors) when setting the rate.

Factors That Affect Personal Loan Interest Rates

There are several factors that lenders consider when determining your interest rate. Understanding these factors can help you secure the best personal loan rate.

- Credit Score:

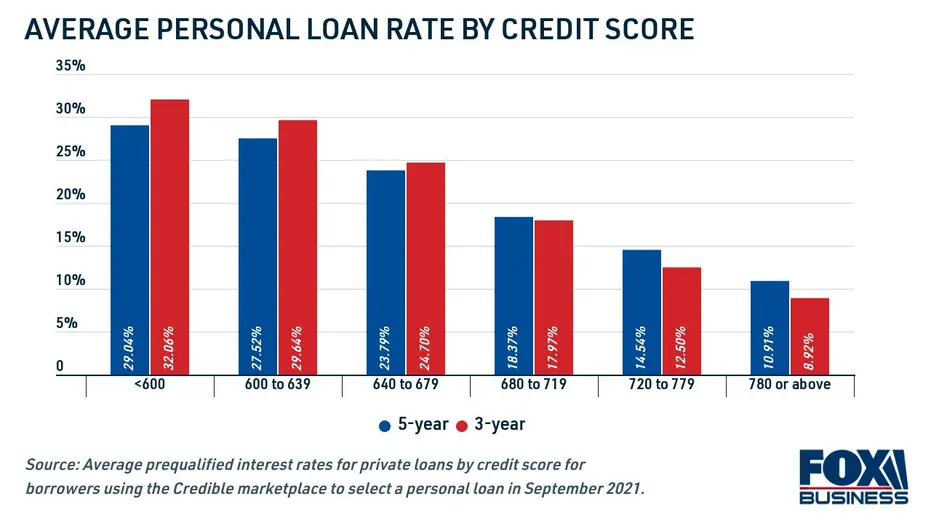

- A higher credit score usually means a lower interest rate. Borrowers with excellent credit (750 and above) tend to receive the best rates, while those with poor credit (below 600) may face higher rates or even be denied.

- Improving your credit score before applying for a personal loan can help you qualify for better rates.

- Loan Amount and Term:

- The loan amount and repayment term can impact the interest rate. Generally, short-term loans (e.g., 1-3 years) have lower interest rates than longer-term loans (e.g., 5-7 years).

- Larger loan amounts can sometimes lead to lower interest rates, but this depends on the lender.

- Debt-to-Income Ratio (DTI):

- Your DTI ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates that you have enough income to handle additional debt, and this may result in a more favorable interest rate.

- Lenders typically prefer borrowers with a DTI ratio under 36%.

- Income and Employment Status:

- Lenders look for borrowers who have stable employment and sufficient income to repay the loan. Providing proof of a steady income can help lower your interest rate, as it reduces the lender’s risk.

- Collateral (for Secured Loans):

- If you take out a secured personal loan (one that requires collateral, such as a car or home), the lender may offer a lower interest rate. The collateral acts as security for the loan in case you default, reducing the lender’s risk.

- Market Conditions:

- Interest rates are also influenced by market conditions. For example, when the central bank raises or lowers interest rates, lenders tend to follow suit, adjusting their rates accordingly.

How to Find the Best Personal Loan Interest Rate

Securing the best possible interest rate on your personal loan can save you a significant amount of money over the life of the loan. Here are some tips to help you find the most competitive rates:

- Check Your Credit Score:

- Before applying for a personal loan, check your credit score to see where you stand. The higher your credit score, the better rate you’ll likely get. If your score is low, consider taking steps to improve it before applying for a loan.

- Shop Around and Compare Lenders:

- Don’t settle for the first loan offer you receive. Shop around with different lenders, including banks, credit unions, and online lenders, to compare interest rates, terms, and fees.

- Use online comparison tools to get an idea of the rates available to you, but ensure that you check specific lender websites for accurate information.

- Consider Loan Terms and Fees:

- While low interest rates are important, don’t forget to consider fees such as origination fees, prepayment penalties, and late fees. A loan with a low interest rate but high fees might not be as cost-effective in the long run.

- Check for Prequalification:

- Many lenders offer prequalification or soft credit checks that allow you to see potential interest rates without affecting your credit score. This can help you narrow down your options before committing to a full application.

- Choose the Right Loan Term:

- Shorter loan terms typically come with lower interest rates, but they also require higher monthly payments. Be sure to choose a loan term that fits your budget and repayment ability.

- Consider a Co-Signer or Secured Loan:

- If your credit is not great, consider applying with a co-signer who has better credit, or consider a secured loan that uses collateral to secure a lower interest rate.

How to Improve Your Personal Loan Interest Rate

If you’re looking to improve your chances of getting a lower interest rate, consider these strategies:

- Improve Your Credit Score: Work on increasing your credit score by paying off debts, reducing credit card balances, and avoiding new credit inquiries before applying.

- Pay Down Existing Debt: Reducing your debt can improve your debt-to-income ratio, making you a more attractive borrower.

- Increase Your Income: If possible, increase your income or add a co-borrower to help demonstrate your ability to repay the loan.

Conclusion

Understanding personal loan interest rates is crucial for finding the best loan terms and minimizing the cost of borrowing. By shopping around, comparing offers, and considering factors like your credit score, loan term, and collateral, you can secure a loan with a competitive interest rate that fits your financial situation.

Remember, the key to getting the best rate is to improve your creditworthiness and consider multiple lenders. With the right research and preparation, you can find a personal loan that helps you achieve your financial goals at a manageable cost.